How do you calculate impairment value

By Sophia Carter

Subtract the fair market value of the asset from the book value of the asset. … Determine if you are going to hold on and use the asset or if you are going to dispose of the asset.

What is impaired value?

An impaired asset is an asset valued at less than book value or net carrying value. In other words, an impaired asset has a current market value that is less than the value listed on the balance sheet. To account for the loss, the company’s balance sheet must be updated to reflect the asset’s new diminished value.

What is impairment example?

Impairment in a person’s body structure or function, or mental functioning; examples of impairments include loss of a limb, loss of vision or memory loss. Activity limitation, such as difficulty seeing, hearing, walking, or problem solving.

How do you find the impairment of an asset?

- Assets are considered impaired when the book value, or net carrying value, exceeds expected future cash flows.

- If the impairment is permanent, is must be reflected in the financial statements.

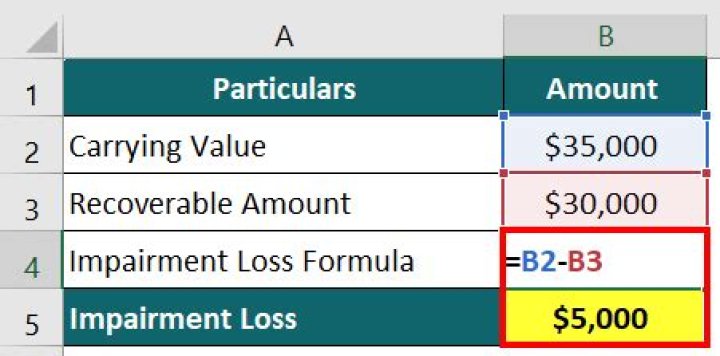

How do you calculate impairment loss under US GAAP?

Impairment loss = asset’s book value – asset’s fair value (or the present value of the future cash flows expected).

How do you calculate depreciation after impairment loss?

Determine the accumulated the depreciation recorded to date on the equipment. Subtract the accumulated depreciation from the original cost of the item. Using straight-line depreciation, calculate the annual depreciation by dividing the original cost by the number of years in useful life.

How do you calculate impairment loss example?

Subtract the future value or present value of any future net cash flows from the book value of the asset, then add back the cost to dispose of the asset if you are going to get rid of it. This is the total impairment loss for an asset you are disposing of.

How do you record impairment of fixed assets?

Accounting for Impaired Assets The total dollar value of an impairment is the difference between the asset’s carrying cost and the lower market value of the item. The journal entry to record an impairment is a debit to a loss, or expense, account and a credit to the related asset.How is value in use calculated?

- The future cash inflows and outflows from continuing use of the asset are estimated.

- The cash inflow from the ultimate disposal of the asset is estimated.

- These cash inflows and outflows are then discounted using an appropriate discount rate.

Perform a recoverability test is to determine if an impairment loss has occurred by evaluating whether the future value of the asset’s undiscounted cash flows is less than the book value of the asset. If the cash flows are less than book value, the loss is measured.

Article first time published onHow do you measure recoverable value?

- If fair value less costs of disposal or value in use is more than carrying amount, it is not necessary to calculate the other amount. …

- If fair value less costs of disposal cannot be determined, then recoverable amount is value in use. [

What is impairment on a balance sheet?

Impairment exists when an asset’s fair value is less than its carrying value on the balance sheet. … An impairment loss records an expense in the current period that appears on the income statement and simultaneously reduces the value of the impaired asset on the balance sheet.

Whats impairment means?

Definition of impairment : the act of impairing something or the state or condition of being impaired : diminishment or loss of function or ability …

How do you allocate impairment loss to assets?

Under IAS 36, impairment losses are allocated first to goodwill and then to the identifiable assets on a pro rata basis. All the impairment loss in the example relates to goodwill and is allocated to the two subsidiaries that form the CGU. The loss will be allocated based on their relative carrying amounts of goodwill.

How do you calculate goodwill impairment loss?

An impairment is recognized as a loss on the income statement and as a reduction in the goodwill account. The amount that should be recorded as a loss is the difference between the asset’s current fair market value and its carrying value or amount (i.e., the amount equal to the asset’s recorded cost).

Where do you record impairment loss on the income statement?

The asset impairment loss on income statement is reported in the same section where you report other operating income and expenses. An impairment loss ultimately reduces the profit your business reports for the period, but it has no immediate impact on the company’s cash balance.

How do you calculate double declining balance depreciation?

Double Declining Balance Method Formula Using the Double-declining balance method, the depreciation will be: Double Declining Balance Method Formula = 2 X Cost of the asset X Depreciation rate or. Double Declining Balance Formula = 2 X Cost of the asset/Useful Life.

How do you calculate the present value factor?

Also called the Present Value of One or PV Factor, the Present Value Factor is a formula used to calculate the Present Value of 1 unit n number of periods into the future. The PV Factor is equal to 1 ÷ (1 +i)^n where i is the rate (e.g. interest rate or discount rate) and n is the number of periods.

How do you calculate values in Excel?

Present value (PV) is the current value of an expected future stream of cash flow. PV can be calculated relatively quickly using excel. The formula for calculating PV in excel is =PV(rate, nper, pmt, [fv], [type]).

How would you calculate the value in use of a CGU?

Value in use equals the present value of the cash flows generated by an asset or a cash generating unit. Impairment loss, if any, under IFRS is determined by comparing the carrying amount of an asset of CGU to the higher of the fair value less cost to sell or the value in use of the asset.

What amount of impairment loss if any should be recognized?

What amount of impairment loss, if any, should be recognized? D. ($100,000,000 carrying value – $80,000,000 fair value) should be recognized.

What is recoverable amount impairment?

Recoverable amount is the higher of (a) fair value less costs to sell and (b) value in use. … An impairment loss is recognised immediately in profit or loss (or in comprehensive income if it is a revaluation decrease under IAS 16 or IAS 38). The carrying amount of the asset (or cash-generating unit) is reduced.

Is impairment an accounting estimate?

They are used in the financial statements to determine the carrying amounts of assets and liabilities and the associated income or expense for the period where such amounts cannot be measured with precision and certainty. Examples of accounting estimates include: … Impairment of non-current assets.

How do you test for impairment of goodwill?

As the new single-step approach for assessing goodwill impairment compares the fair value and carrying value of the entire reporting unit, the goodwill impairment charge (if any) may capture fair value declines, below their carrying values, for non-goodwill assets.

What is an impairment loss in accounting?

The technical definition of the impairment loss is a decrease in net carrying value, the acquisition cost minus depreciation, of an asset that is greater than the future undisclosed cash flow of the same asset.

Does impairment affect net income?

An impairment loss makes it into the “total operating expenses” section of an income statement and, thus, decreases corporate net income.

Which method is used for testing impairment?

The fair-value test determines the impairment loss for an indefinite-life intangible asset as the amount by which the carrying value of the asset exceeds the fair value of the asset.

Is impairment loss tax deductible?

In general, tax authorities attempt to tax company income as close to its cash base as possible, rather that its accrual base. This means tax authorities do not allow impairment as a deductible expense to taxable income because impairment expense is not connected to a sale or purchase in the accounting period.

What is recoverable value?

Recoverable amount is the greater of an asset’s fair value less costs to sell, or its value in use. … Thus, the concept essentially focuses on the greatest value that can be obtained from an asset, either by selling or using it.

How frequently should assets be tested for impairment?

Intangible assets with an indefinite useful life are required to be tested annually for impairment irrespective of whether there is an indication that they may be impaired (see section 6).